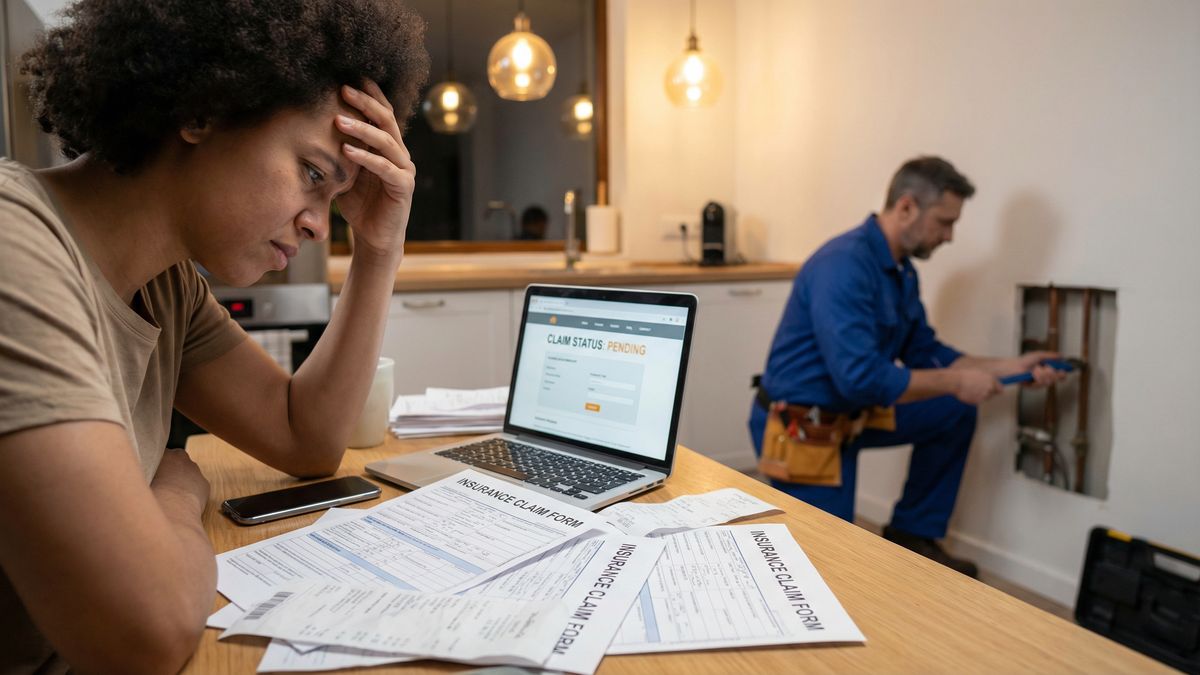

That sinking feeling hits you. You see a puddle on the floor that has no business being there, or maybe your water bill just shot through the roof. You have a classic warning sign of a slab leak, and the initial panic about the damage is quickly followed by a second wave of dread: dealing with your insurance company.

It feels like you're about to walk into a high-stakes game where you don't know the rules. You've heard the horror stories from friends or neighbors. Stories about claims getting denied over a technicality, leaving them with thousands of dollars in repair bills. The fear of saying the wrong thing or making one small mistake that costs you everything is completely overwhelming.

But you don't have to go through this blind. What if you had a clear roadmap from a team that deals with this every single day? We're going to walk you through the exact steps to take to navigate your slab leak insurance claim, avoid the common pitfalls, and give you the best possible chance of getting it approved.

Your First Call Can Make or Break Your Claim

Before you even think about calling a plumber to start tearing up your floor, you need to make a different call. Your very first action should be to contact your insurance agent and report the potential claim. This is non-negotiable.

Why? Because your insurance provider needs to send their own adjuster to assess and document the situation. If you start repairs before they see the initial damage, they can argue they can't verify the cause or extent of the problem. This can lead to an immediate denial, and you don't want to start from that position.

Document Everything Like a Forensic Investigator

This is the most critical piece of advice we can give you. Before anything is moved, cleaned up, or repaired, document everything. Get out your phone and take more photos and videos than you think you need. Get close-ups of the water damage, wide shots of the affected rooms, and videos where you walk through the area and narrate what you're seeing.

This documentation is your proof. It is the primary evidence you will have to support your claim. There is no such thing as too much evidence in this situation. This visual proof is invaluable when the adjuster reviews your case.

The Golden Rule: Understanding Your Coverage

Here is the single most misunderstood part of a slab leak insurance claim. Your homeowner's policy typically covers the resulting damage from the water, but not the cost to repair the broken pipe itself. It's a crucial distinction.

So, the policy might cover the cost to dry out your home, replace your ruined flooring, and repair drywall. However, the cost of the actual plumbing work to fix the leak, whether it's a spot repair or a more complex reroute, often falls on you. Knowing this upfront helps you set realistic expectations. For a deeper dive, read our guide on how insurance coverage for slab leaks works.

Get a Professional Leak Detection Report

After you have the go-ahead from your insurer, your next step is to hire a specialist for professional leak detection. This isn't a job for a general handyman. A specialist will use electronic equipment to pinpoint the exact location of the leak without needlessly damaging your property.

They will provide you with a formal, written leak detection report. This document is gold. It provides the specific, technical details your insurance company needs to validate the claim. It moves your situation from a vague "I have a leak" to a documented "the leak is located here, and this is the cause."

Don't Be Afraid to Push Back on a Denial

If your claim is denied, don't just accept it. Insurance adjusters are human, and sometimes they make mistakes or interpret policies in the company's favor. You have the right to appeal their decision.

Start by carefully reading the denial letter to understand their exact reason. Compare this with the language in your policy and the evidence you gathered. If you have a solid case with a professional leak detection report, you are in a strong position to challenge the denial. Sometimes, simply showing you are prepared and informed is enough to get them to reconsider.

The Ultimate Solution: Preventing Future Claims

Going through a slab leak and an insurance claim is a stressful experience you never want to repeat. Once the immediate crisis is over, it's time to think long-term. If your home has older, deteriorating pipes, this single leak might just be the first of many. This is a topic we cover in our complete guide to slab leaks.

This is where a whole house repipe becomes the definitive solution. By replacing the old, unreliable plumbing under your foundation with new, durable pipes, you eliminate the root cause of slab leaks. Not only does this prevent future water damage and insurance headaches, but it can also lower your homeowner's insurance premiums. It's a smart investment in your property and your peace of mind. Curious about the investment? We break down the cost of repiping a house in Las Vegas.

Claim Denied? Get a Second Opinion.

If your insurance denied your slab leak claim, don't give up. Call us. We'll provide the professional documentation and assessment you need to fight back.

Call or Text (702) 605-6169 Book Your Appointment Online